In 2010, the scale of China's semiconductor lighting industry was 120 billion yuan. Although the good development momentum at the end of 2010 did not continue as expected in the industry in 2011, many companies have unsatisfactory operating conditions, and even some companies have closed down, but it is undeniable that China's semiconductor lighting industry base is still being further consolidated and remains the fastest growing region in the world. In 2011, the scale of China's semiconductor lighting industry reached 156 billion yuan. It is expected that during the “12th Five-Year Plan†period, the overall scale of China's semiconductor lighting industry will increase by 30%. In 2015, the scale of domestic semiconductor lighting will reach 500 billion yuan.

In 2010, the scale of China's semiconductor lighting industry was 120 billion yuan. Although the good development momentum at the end of 2010 did not continue as expected in the industry in 2011, many companies have unsatisfactory operating conditions, and even some companies have closed down, but it is undeniable that China's semiconductor lighting industry base is still being further consolidated and remains the fastest growing region in the world. In 2011, the scale of China's semiconductor lighting industry reached 156 billion yuan. It is expected that during the “12th Five-Year Plan†period, the overall scale of China's semiconductor lighting industry will increase by 30%. In 2015, the scale of domestic semiconductor lighting will reach 500 billion yuan. The semiconductor lighting industry is considered to be an important means of transforming the economic development mode, adjusting the industrial structure, stimulating the development of related industries, and achieving sustainable development. It is also one of the most promising strategic emerging industries in the 21st century. With the rapid development of technological progress and market applications, the semiconductor lighting industry has a very broad prospect. First of all, as the biggest source of development for semiconductor lighting at present, the application of liquid crystal (LCD) backlighting, lighting, and other fields is proceeding very rapidly and with huge space. At the same time, the rapid development of LED innovation applications, with the formation of applications in the fields of agriculture, health care, information intelligence networks, aerospace, etc., LED will become a pillar industry with a trillion yuan scale.

During the "Eleventh Five-Year Plan" period, the compound growth rate of China's semiconductor lighting industry reached 35%, becoming the fastest growing region in the world. In 2010, the scale of China's semiconductor lighting industry was 120 billion yuan. Although the good development momentum at the end of 2010 did not continue as expected in the industry in 2011, many companies have unsatisfactory operating conditions, and even some companies have closed down, but it is undeniable that China's semiconductor lighting industry base is still being further consolidated and remains the fastest growing region in the world. In 2011, the scale of China's semiconductor lighting industry reached 156 billion yuan. It is expected that during the “12th Five-Year Plan†period, the overall scale of China's semiconductor lighting industry will increase by 30%. In 2015, the scale of domestic semiconductor lighting will reach 500 billion yuan.

A, LED packaging industry situation and trend <br> <br> as part of the middle reaches of the industrial chain of semiconductor lighting, LED device package plays a connecting role in the development of semiconductor lighting industry in China and also the division of labor in the global semiconductor lighting industry chain One of the industry links with scale advantages and cost advantages.

According to Strategies Unlimited, the market size of bright LED in 2010 reached US$10.8 billion. Although the growth in market demand in 2011 failed to meet industry expectations, from the sales point of view, although the market size will not have significant growth, the packaging of LED devices will still have a large increase.

In 2011, the scale of China's LED packaging industry reached 28.5 billion yuan, an increase of 14% from 25 billion yuan in 2010, and the output increased from 133 million in 2010 to 182 billion, an increase of 36%. In terms of the global LED packaging industry, China is already the most concentrated region in the global packaging industry and the main grounding for the global LED packaging industry transfer. China and Taiwan, as well as the United States, South Korea, Europe, Japan and other major LED companies have very good packaging capabilities Most of them are realized in mainland China. At present, there are more than 1,500 packaging companies in China, focusing on small and medium-sized enterprises in the low-end market. There are not many companies that truly have economies of scale and international competitiveness.

With the continuous promotion of applications such as backlight and lighting, the market demand for LEDs is constantly changing. As far as the packaging structure of LED devices is concerned, the current main package types include lamp LEDs, surface mount packages (SMD LEDs), high power LEDs, and chip-on-board (COB) packages. Types of. For the current and future market demand, backlight and lighting will become the most important applications, the demand for LED devices will be based on SMD LED, High Power LED and COB. As far as the quality of LED devices is concerned, the requirements for LED reliability, light efficiency, and service life are getting higher and higher. Small-scale and low-level packaging companies cannot meet the quality requirements of LED applications. The domestic LED packaging capacity is presented. With regard to the trend of concentration, the leading enterprises in the domestic packaging industry are rapidly improving their productivity and automation.

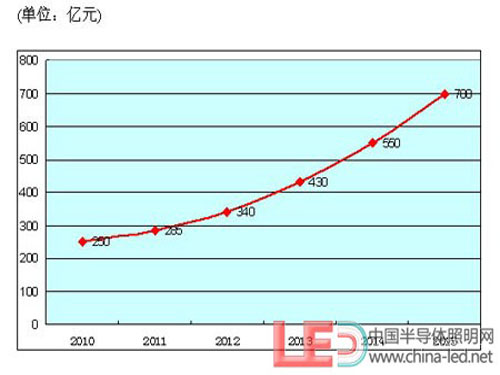

Figure 1 Domestic LED package output forecast Source: National Semiconductor Lighting Engineering R&D and Industry Alliance (CSA)

It is expected that China's LED packaging will maintain a high growth rate in the coming years. In 2015, China's LED packaging output value will reach 70 billion yuan, and the compound annual growth rate of the entire package will be about 40%.

Second, LED packaging equipment demand characteristics analysis <br> <br> With the scale of China's leading enterprises to gradually expand the package, as well as many packaging companies in the Stock Exchange public offering of listed issuers, industrial concentration of LED packages, a single enterprise scale and automation There will be a greater degree of improvement. With the change of the LED packaging industry, the demand for LED packaging equipment also has some prominent features.

First of all, the demand for LED packaging equipment, especially automation equipment, has rapidly increased in China and has become the largest demand area for global packaging equipment. From the perspective of the sales region of the world's largest LED packaging equipment manufacturer, ASM's turnover in mainland China accounted for 33.6%, 37.6%, and 44.8% of its total turnover in 2009, 2010, and 2011, respectively. It is also the fastest. From one aspect shows the mainland in the LED packaging equipment market status and development potential.

Second, LED equipment has always been a weak link in the development of China's semiconductor lighting industry. LED packaging equipment is no exception. As of the end of 2010, there are nearly 130 LED packaging equipment manufacturers worldwide, of which about 100 have been deployed in China, accounting for 76.9% of the world's total. In the domestic market, ASM occupies 28.7% of the market share, with manufacturers from Japan and Taiwan accounting for 25.8% and 15.2%, respectively, with European and American manufacturers taking up 10.3%; domestic equipment manufacturers account for 20%. In 2011, there was a notable increase in domestically-made equipment, but there were still about 70% of equipment. The main reason was that automation equipment relied on imports. LED packaging main production equipment is a solid crystal machine, wire bonding machine, dispensing machine, sealing machine, splitting machine and automatic tape dispenser. Judging from the current domestic equipment situation, the sealer has been successfully domesticated with excellent performance and can meet industry requirements. Solid crystal machines, wire bonders, dispensers, splitters, and automatic taping machines are also mainly imported, but in recent years, the level of domestic equipment has also been continuously improved, especially solid crystal machines and welding. The localization rate of line machines and other equipment has increased rapidly, and a number of leading companies have also emerged, such as Shenzhen Cuitao Automation Equipment Co., Ltd., whose sales of solid crystal machines reached 600 in 2011, accounting for 18% of the domestic market in terms of quantity. About 30% of the domestic solid crystal machines.

Third, the high degree of automation, rapid speed, high precision, and the overall solution of the entire production line have become the hot spots for LED packaging equipment. With the improvement of domestic LED product quality requirements and the rapid increase in domestic labor costs, the demand for equipment is characterized by faster speed, higher accuracy, better stability, and higher level of automation. The more prominent point is that with the increase in the size of packaging companies and R&D capabilities, the R&D and design capabilities of LED devices are also rapidly increasing. Specific products require devices with specific functions, and full-line device solutions for LED packaging companies are required. The demand for solutions and customized equipment has greatly increased.

Three, LED packaging equipment competition <br> <br> equipment industry has been the core industries and high-value industrial sectors, is also typical of technology, capital-intensive industries, the main competition in one of the few companies to start. From the perspective of the global value chain of the packaging equipment industry, developed countries mainly intercept high-value-added segments, and are known for their core raw material manufacturing technologies, motion control and visual imagery, process management, intellectual property protection, and brand management, such as high-end products in the industry. It is mainly supplied by the United States, Japan, and Switzerland, which have the most advanced packaging equipment manufacturing technologies in the world. At present, China still has a large gap between the R&D and manufacturing of core equipment for packaging and foreign companies. The equipment supplied is mainly concentrated on crystal-fixing machines, low-precision wire bonders, and post-process related equipment types with low technological content. There are only a few high-precision wire bonders in China, and the entire LED packaging equipment industry is climbing up from the bottom of the industrial value chain.

As of the end of 2010, there are more than 130 LED packaging equipment manufacturers worldwide, including about 100 domestically, accounting for a global 76.9% of the number of manufacturers, to achieve a 20% share of the domestic LED packaging equipment market, and the product lines are mainly concentrated in the low-end Equipment market. The industry concentration in high-end product areas is relatively high. Foreign companies have strong technical strength and are monopolized in certain areas. This fully illustrates the current market demand for LED packaging equipment industry in China, the small scale of the company, the incomplete product line, and the low level of technology.

However, it is worth noting that domestic equipment started late, but it has developed rapidly. Especially in recent years, with the increase in the scale and level of China's LED packaging industry, driven by the domestic market demand, China's LED packaging equipment industry has made rapid progress. Domestically-priced equipment with high cost performance has occupied a place in the packaging equipment market. The technologies, equipments, products and brands of domestic leading enterprises already have certain global competitiveness. For instance, Shenzhen Cuitao Automation Co., Ltd. is specialized in wire bonders, solid crystal machines, and dispensers. Optoelectronics in photoelectric detection equipment and so on.

Before 2008, China's LED automation packaging production equipment was basically monopolized by European, Japanese and Taiwanese manufacturers. By 2010, the country’s LED automation equipment has accounted for about 20% of the market share. In 2011, the domestic equipment market share exceeded 30%. , China's LED packaging equipment is entering the golden period of development. At the same time, with the rapid growth of domestic demand, a group of domestic companies have passed the difficult period of R&D investment, proposed a complete new technology and new product R&D innovation system, and launched a series of equipment with international standards, such as Cui Tao Automation. , Dazu Laser, Hangzhou, Hangzhou Zhongwei etc. For specific equipment, the domestic industry level and major suppliers are shown in Table 1.

Fourth, LED packaging equipment market demand outlook In 2011, although the overall situation of semiconductor lighting and expectations have a big gap, in 2011 the market scale of equipment growth is also the lowest in recent years, but from the overall development of the semiconductor lighting industry Look, the trend of rapid development of semiconductor lighting has not changed, the trend of China becoming a global LED packaging base has not changed, the scale and automation trend of LED packaging industry has not changed, the market demand for LED packaging equipment in China will remain high in the next few years With the growth rate, the compound annual growth rate of China's LED equipment demand by 2015 will be around 24%. Thanks to the price and service advantages of domestic equipment, more importantly, with the continuous improvement of China's equipment manufacturing level, domestic equipment will gradually occupy the leading position in the domestic demand for LED equipment, and domestic equipment manufacturers that are rapidly developing will also be The LED equipment market is in a competitive position.

Considering the impact of LED packaging product composition, automation level, production capacity increase and equipment renewal in China, according to the calculations of international semiconductor lighting engineering R&D and industrial alliances, the market demand for LED packaging equipment in China will reach 17.2 billion yuan in 2015. ,as shown in picture 2.

Domestic LED packaging equipment demand forecast Source: National Semiconductor Lighting Engineering R&D and Industry Alliance (CSA)

In the future competition of LED packaging equipment, according to the development experience of the international equipment industry, the degree of industrial concentration in the country will further increase. The key core equipment such as die-bonding, bonding wire, and split-light separation will occupy a large number of companies. Part of the market share situation. R&D capabilities and product improvement capabilities will become the most critical competitive factors for LED packaging equipment companies. Only companies with strong research and development capabilities can have advantages in future competitions, such as Cui Tao Automation, Han Optoelectronics, Zhongwei Optoelectronics, etc. The higher proportion of companies is most likely to become the dominant domestic LED device production.

Connecting Terminals,Micro Connecting Terminal,Aluminum Connecting Terminals,Connecting Copper Terminal

Taixing Longyi Terminals Co.,Ltd. , https://www.longyicopperterminals.com