This report analyzes the development background, development status, industrial chain structure, and development trends of OTT advertisements in order to provide reference for the industry.

The main points of the report:

1. In 2016, the number of OTT subscribers in China has reached 140 million. The dramatic increase in attention of OTT users brought about by the increase in the number of OTT subscribers is the fundamental driving force for the development of OTT advertising.

2. Agents and resource-based parties cultivate the market, and advertisers who hold advertising budgets promote it, which means that OTT advertising is truly ushering in great development.

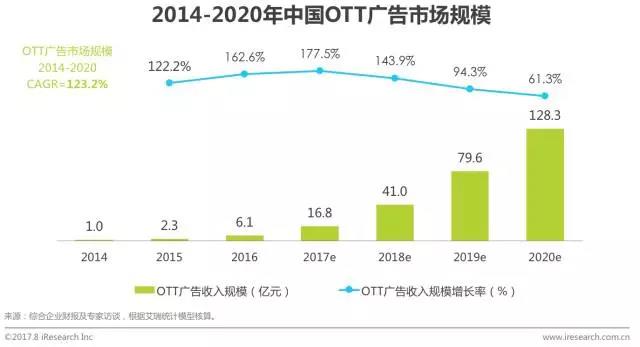

3. In 2016, the size of China's OTT advertising market was 610 million with a growth rate of 162.6%. With advertisers investing more budget in 2017, OTT advertising will usher in explosive growth. It is estimated that by 2020, the size of China's OTT advertising market will reach 12.83 billion yuan. .

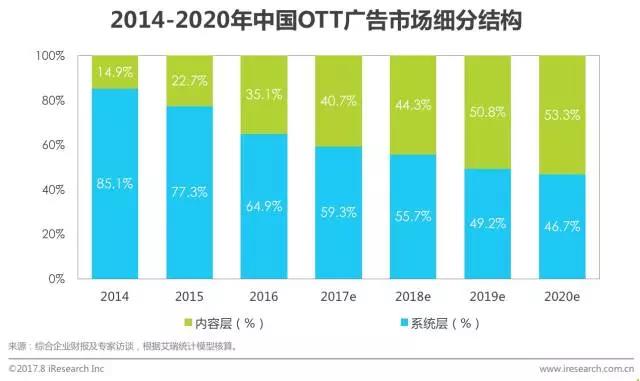

4. In 2016, the subdivision structure of China's OTT advertising market was divided into two major categories: system-level advertising represented by switch-machine advertising and content-level advertising represented by patch advertising. In 2016, system-level advertising accounted for a relatively large amount of 64.9. %, the proportion of content-based advertising is on the rise. It is expected that by 2020, the percentage of content-level advertising will reach 53.3%.

I. Development Background of China's OTT Advertising Market

OTT terminal and OTT advertising concept definition

The OTT terminal uses the public Internet as the transmission medium, and uses the television with the specified number and network access function as the output terminal. The OTT terminal is an integrated broadcast control platform approved by the State Administration of Radio and TV to provide video to users throughout the country. On-demand content services and other related value-added services for television and box terminals.

OTT advertising refers to advertising communication activities based on the public Internet and using OTT terminals as its medium.

Network speed, terminal popularity, user growth, and technology development

The development of OTT advertising has been promoted by many factors. 1) The increase in high-speed broadband coverage has laid the foundation for the popularity of OTT terminals; 2) The increase in the number of OTT terminals, OTT TV has become the mainstream of TV development; 3) The performance of OTT terminals has improved. Features such as large-screen, high-definition, and curved surfaces bring better user experience; 4) OTT users grow in size, with 140 million users in 2016, OTT terminals gradually becoming new family entertainment centers; 5) Technological development, advertising development , launch, monitoring, etc. made progress. At the same time, the development of OTT advertising has also been affected by policies, although at present, the relevant part does not directly supervise OTT advertising, but it affects the OTT advertising market through the OTT terminal and content monitoring policies.

Steady growth in box ownership, TV will be the future mainstream for OTT terminals

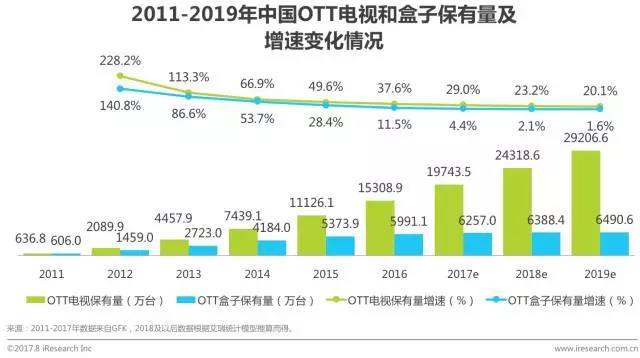

According to the GFK data, China’s OTT TV and box inventory maintained rapid growth between 2011 and 2016, with a CAGR of 88.9% in five years. By 2016, OTT TV capacity was 153.089 million units and OTT box capacity was 59.911 million units. , OTT terminal cumulative total of more than 200 million units. Ereli's analysis believes that OTT TV has become the main choice for users to upgrade, and it is expected that the OTT TV inventory will continue to grow steadily over the coming period, while the OTT box inventory growth will slow down.

In 2016, the number of users reached 140 million, gradually becoming a new family entertainment center

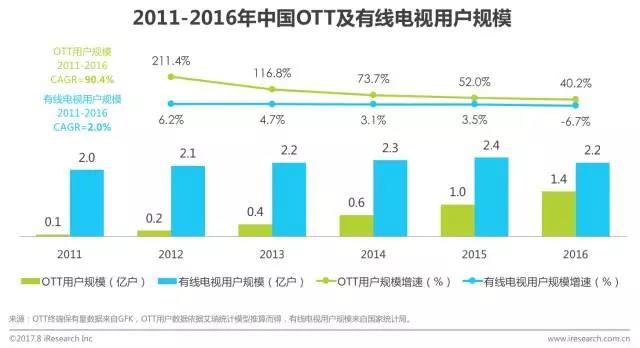

The number of OTT users in China continued to increase between 2011 and 2016. In the five years, the CAGR was 90.4%. By 2016, the number of OTT users reached 140 million. At the same time, according to the data of the National Bureau of Statistics, China’s cable TV The user CAGR was only 2.0%, and it first fell in 2016. Ereli's analysis believes that the decline in the size of cable TV subscribers will be an irreversible trend. OTT terminals will take over the functions of cable TV as a user's home entertainment and become a new family entertainment center.

Advances in ad development, delivery, monitoring, etc. also face challenges

In the process of OTT advertising development, technology is the biggest productivity. Under the circumstance that the terminal manufacturers are scattered, the hardware models are complex, and advertising monitoring is difficult, the parties to the industry chain work together to complete the development, deployment, and monitoring of advertisements. And so on, making OTT advertising run from being able to run up and running fast. At present, the biggest technical difficulty lies in data access. According to Ereli's analysis, as OTT advertising industry parties increase investment in OTT advertising, technology will not become a limiting factor in the development of OTT advertising. The next step is to implement OTT advertising. Programmatic purchases and performance assessments will still play an important role.

Direct supervision of OTT advertisements, affecting the advertising market by monitoring terminal content

Since the OTT terminal was born, it has been the focus of policy supervision. From 2007 to the end of the decade, the SARFT as the core regulatory agency has announced dozens of regulatory requirements, and adopted Circular 56 (2007) and Circular 181 (2011). Year (November) and Order No. 6 (2016) confirmed the access, operation, and supervision modes of the entire OTT market. Ereli's analysis believes that the core goal of the policy is to ensure that the OTT side is manageable and controllable.

At present, relevant departments do not directly supervise OTT advertising. However, OTT terminals and content monitoring policies affect the OTT advertising market. As a whole, the policy has a normative effect on OTT advertisements. From the perspective of policy expectations, Ereli believes that the future of policies The impact on OTT advertising will be mainly reflected in the review of advertising qualifications and the supervision of advertising content. Although there may be some restrictions, it will not hinder the development of OTT advertising.

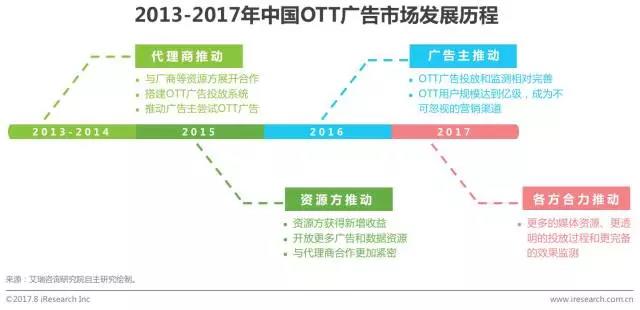

From agency promotion to resource promotion, to advertiser promotion

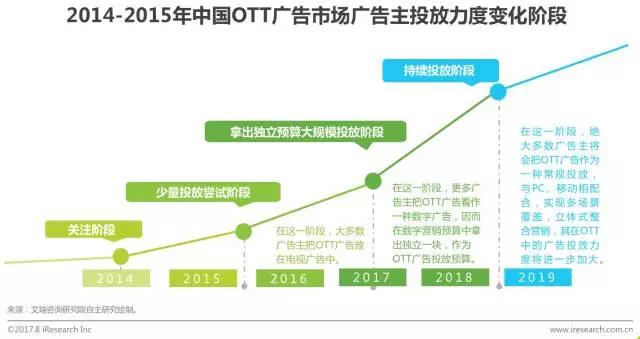

The smart TV box products released in 2012 opened the prelude of the OTT market, which became the basis for the development of the OTT advertising market: 1) Since 2013, there have been agents entering the OTT advertising market, building advertising systems, and other media resources such as manufacturers. The parties launched cooperation to promote advertisers to try OTT advertisements, and the entire OTT advertising market was in the agency promotion stage; 2) In 2015, with the promotion of agents, the media resources parties gained in addition to the original hardware revenue as incremental revenue. Advertising revenue began to focus on the OTT advertising market, working more closely with agents and opening up more advertising resources. During this period, the OTT advertising market was promoted by the media resources. 3) In 2016, the delivery method and monitoring methods of OTT advertisements. Gradually mature, OTT-end users also exceeded 100 million, becoming a marketing battlefield that cannot be ignored. Advertisers began to actively promote the development of the OTT advertising market; 4) Entering 2017, all parties in the industry chain have realized the value of OTT advertising and have begun to work together. To promote market development, Ereli analysts believe that at this stage, advertisers are still the core driving force, and only advertisers do not OTT delivery end budget increase, OTT advertising market can really usher in rapid development, and promote the increased budgets of advertisers, media depends more resources, more transparent and more complete delivery process monitoring results.

Second, the development status of China's OTT advertising market

High reach at the system level and high standardization at the content level

At present, there are two major types of OTT advertisements. One is system-level advertisements, and the other is traditional system advertisements and innovative system advertisements. The system-level advertisements are based on the OTT operating system and are owned by terminal manufacturers, among which traditional system-level advertisements. Represented by switch advertising, CPT and CPM are mostly used for sale. Innovative system-level advertisements are collaborated in a customized manner. Prices vary according to the type and difficulty of the project; the other is content-level advertising. The advertising is based on video content and is represented by patch advertisements. Terminal manufacturers, licensees, content providers, and application developers all have this advertising resource, which is mainly sold through CPM.

Characteristics of OTT advertising: strong exposure, high impact, multiple forms, orientation

The OTT terminal is essentially a TV + Internet + smart operating system. Therefore, OTT advertising combines the dual advantages of traditional TV advertising and Internet advertising: 1) The advantages of strong exposure, high impact, and small interference of traditional TV advertising; 2) The advantages of Internet advertising are programmatic purchase, easy-to-measure and precise targeting.

In 2017, ushered in explosive growth, the market size of 2020 will exceed 12 billion

According to iResearch, from 2014 to 2016, the OTT advertising market grew rapidly. In 2016, the market scale reached 610 million yuan, with a growth rate of 162.6%. Ereli's analysis believes that with the rapid growth of OTT users, OTT advertising industry chain With more and more perfect, advertisers will invest more budget on OTT in 2017, and OTT advertising market will usher in explosive growth. It is estimated that by 2020, the size of China's OTT advertising market will reach 12.83 billion, and the average annual compound growth rate will exceed 123.2%.

System-level advertising has a higher proportion, and the proportion of content layers is on the rise

According to iResearch's data, the OTT advertising market segmentation structure is mainly divided into two major categories: the content layer and the system layer. In 2016, the system layer accounted for 64.9%, and the proportion of content-level advertisements showed an upward trend. According to the analysis, by 2019, as the OTT terminal growth enters the saturation stage, system-level advertising growth will also slow down. As users continue to grow content consumption on the OTT side, content-based advertising will continue to grow rapidly, exceeding system-level advertising for the first time. It is expected that by 2020, the percentage of content-level advertisements will reach 53.3%.

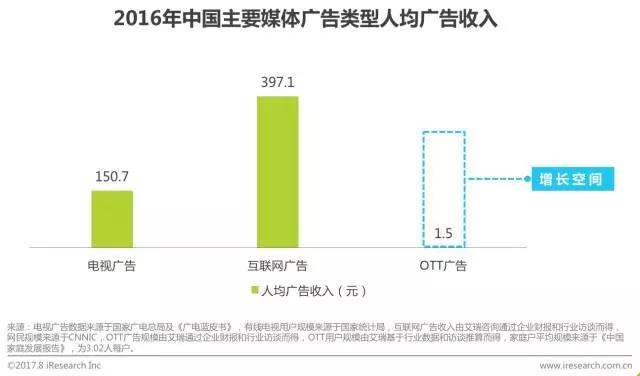

At present, the value of OTT advertising is far from being tapped, which has huge potential for growth

According to iResearch, in 2016, TV advertising revenue per capita was RMB 150.7, and per-person advertising revenue from Internet advertising was RMB 397.1. Compared with per capita advertising revenue of OTT advertising, it was only RMB 1.5. According to Ereli's analysis, on the one hand, OTT advertising The initial stage of commercialization is at an early stage and the overall scale is still small; on the other hand, it also reflects that OTT advertising has been seriously underestimated and its value has not been tapped. Based on OTT advertising itself, it combines TV commercials and Internet advertising. With its many advantages, Ereli believes that the reasonable per capita advertising revenue of OTT advertising exceeds the per capita income of television advertising at least, and therefore its growth potential is huge.

III. Analysis of China OTT Advertising Market Industry Chain

OTT advertising market industry chain map

Advertiser: From paying attention to trying, to come up with independent budget, increasing attention to OTT advertising

From the perspective of the entire industry chain, the advertiser’s budget determines the size of the OTT advertising market. At present, brand advertisers are the main players in OTT advertising. This is affected by both the characteristics of OTT advertising and the self-demand of brand advertisers. , OTT advertising has a strong exposure, high touch advantage, more able to attract brand advertisers with a large number of product demand; on the other hand, brand advertisers generally prefer video format advertising, its past in television advertising and OTV advertising The large amount of experience accumulated during the launch prompted them to be more willing to promote the delivery of OTT advertisements. In the past three years, brand advertisers have experienced OTT advertisements, followed by a small amount of delivery attempts and come up with three stages of independent budgets. In the next step, OTT will serve as the regular media for advertisers and enter the continuous delivery phase.

Advertisers: The growth potential of traffic, finance, and local advertisers on the OTT side

Among many brand advertisers, iResearch data shows that from January to July 2017, food and beverages, internet services and make-up bathroom products were the top three industries with the largest share of OTT advertising, including food and beverages and make-up baths. The category is basically advertisers for fast elimination. IResearch believes that there are three reasons why fast-moving advertisers favor OTT advertising: 1) Fast-disposal advertisers have a large marketing budget and high marketing demand; 2) New marketing forms and marketing media acceptance and willingness to try are relatively high. It is an important advertiser of all major media; 3) OTTs that are in a family context are more in line with the decision-making and consumption scenarios of fast-eliminating products.

According to iResearch data, compared with PC and mobile advertising, OTT traffic, financial and other industries accounted for a relatively low proportion, iResearch analysis, OTT ads high reach, large exposure, strong impact characteristics and their families The scene is also very suitable for traffic advertisers. In the next year or two, the proportion of placing share will increase. At the same time, financial and local advertisers have a larger growth potential.

Marketing service providers: get good media resources, serve advertisers is still the core competitiveness

Every time the transfer and rise of Internet traffic will bring new opportunities for marketing service providers, from PC to mobile, in just five years, the mobile terminal has grown from scratch, from budding to highly mature, and now, marketing services. The window period for mobile terminals on the mobile side has passed, and the OTT advertising market has become their new point for the Nuggets. Currently, there are two main types of efforts in the field of OTT advertising: 1) Marketing service providers transformed from TV, PC and mobile all the way They rely on the past customer resources and industry experience; 2) The marketing service providers who started from OTT, their advantage is to enter the market early, deeper understanding of the market, and accumulated a wealth of practical experience, they hope in the overall situation When it is undetermined, you can win the opportunity and take a place.

Ereli's analysis believes that in the OTT advertising market, the business logic and competitive strategy of marketing service providers have not fundamentally changed. For the marketing service providers, expanding industry customers and media resources is still their core competitiveness. Therefore, we can see that since 2016, marketing service providers have established cooperative relationships with media resource parties and advertising monitoring parties, and have vigorously promoted advertisers to put them on the OTT side.

Media Resource Party: Get more users through upstream and downstream resource cooperation to enhance liquidity

In the OTT advertising industry chain, terminal manufacturers, licensees, content parties, and application developers all have media resources, and the parties will also cooperate through SDK pre-installation, resource agency, and advertising distribution. In the media resources side, the licensee is a partner that cannot be bypassed by both the terminal manufacturer and the content provider. For the terminal vendor, having more content partners means more content, attracting users to purchase terminal products, and thus acquire Hardware revenue and advertising revenue; For content parties, working with more terminal vendors to quickly increase their content coverage means more traffic, thus increasing liquidity and higher income.

IV. Development Trend of China's OTT Advertising Market

Trend 1: Users sink and continue to grow

Leading the market to increase customer ARPU, increase and potential market to expand new customers

At present, as OTT terminals are distributed in coastal provinces and first and second-tier cities, OTT advertising is more concentrated. Ereli's analysis believes that with the growth of OTT terminals in the coastal provinces and first and second-tier cities tends to be saturated, the third and fourth tier cities have become the focus of OTT terminal manufacturers, which will promote the development of OTT advertisements in third and fourth tier cities. Divided into leading market, rising market and potential market, within the next three years, in the leading market, the OTT advertising resource party and the agent's strategy focuses on maintaining old customers and increasing customer ARPU, while on the up market and potential market, OTT advertising Resource and agent should pay more attention to acquiring new customers.

Trend 2: Multi-screen interaction, multi-screen marketing

Based on routing IP, device ID, and QR code to derive more ways to play

In most cases, there will be more than one connected device in the home scene where the OTT advertisement is located. This brings many possibilities for multi-screen interaction and multi-screen marketing: 1) Networked devices in the same network condition in the home include: Computers, tablets, mobile phones, televisions, etc., can identify connected devices in the same home based on the same IP, and provide the basis for subsequent multi-screen interactions; 2) Implement cross-screen user tracking by matching different device IDs, and study users in different device terminals. The behavior is to formulate a multi-screen marketing strategy more scientifically; 3) to achieve user-end multi-screen interaction through two-dimensional codes, shake, etc., to enhance the playability and conversion effects of OTT advertisements.

Trend 3: Form Diversification, Content Primitive

Inventory resources and degree of standardization are key factors in considering new forms of market space

Because it is still in the early stage of commercialization, the current OTT advertising format is relatively simple, with the commercialization of the OTT end, the advertising needs of the OTT end of the advertising market and OTT advertising technology maturity, especially the application of artificial intelligence technology, OTT advertising market will More innovative advertising formats and content emerged. Ereli's analysis believes that inventory resource richness and standardization degree are key factors in considering the new advertising market space. Based on these two factors, Ereli believes that OTT-side video advertising and post-implantation Advertising has more development potential.

Trend 4: Programmatic Acceleration

Supported by DMP, PDB and PMP are the main purchase methods

Although OTT advertising is currently dominated by traditional purchasing methods, Ereli's analysis believes that in the future, the delivery of OTT advertisements will surely be different from the one-to-many aspect of traditional TV advertising, and real-time media, crowds, and creativity will be realized through programmatic purchases. Automation. Of course, the implementation of OTT-side programmatic purchase is also faced with certain difficulties: 1) Reliance on IP address for geographical orientation, due to changes in IP and the same cell sharing the public network IP, there is an error in accuracy; 2) with PC, Mobile Different from individuals, OTT takes the family as the unit. There are great differences in the age, gender, and interests of family members, and it is difficult for users to target. Ereli's analysis believes that in the face of these challenges, the industry is already constructing methodologies and achieving phased results. With the implementation of these practices, these problems will be gradually solved. In the future, from the point of view of purchase methods, OTT will Mainly brand advertising, OTT-side programmatic purchase will be based on PDB, PMP and other methods.

Trend 5: Voice Advertising Potential

Voice interaction has become the mainstream OTT interaction method, bringing more possibilities for voice advertising

In the development of home TV, the interaction between users and TV has also been iterative. From the early remote control to the later mouse and keyboard, and nowadays, voice interaction has increasingly become the mainstream interaction method. In the future, somatosensory interaction will also become important. Assist interactive mode. Ereli's analysis believes that the popularity of voice interaction will bring more possibilities for voice advertising. The voice advertising behind it depends on artificial intelligence technology such as speech synthesis, speech recognition and semantic understanding. The directions that voice advertisements can try include keyword advertisements, question and answer advertisements, broadcast advertisements, and the like. Voice advertising is more fresh, interactive, and playable, but with great development, it is necessary to standardize voice advertising and find suitable entry scenarios.

Trend 6: OTT-end advertising monitoring is more complete

Gradually cover the three stages of advertising before, during and after

From the perspective of advertisers, the completeness of OTT advertising effectiveness monitoring is a necessary condition for advertisers to increase budgets on the OTT side. At the OTT side, third-party monitoring companies have started to provide advertisers with some monitoring services. In the future, IResearch believes that The monitoring of advertising effectiveness will gradually cover the three stages of advertising before, during and after the launch of the advertisement. 1) Prior to the launch, historical advertising monitoring data will be used to help advertisers estimate the effectiveness of advertisements and guide them in formulating their delivery strategies; 2) During delivery, advertisers can track ad delivery performance in real time to help advertisers optimize their ad delivery behavior and avoid wasting unnecessary budgets during the delivery process. 3) After launch, fully evaluate the effectiveness of the delivery, measure input and output, and provide follow-up performance. Gain experience.

Aluminum Laptop Cooling Stand,Aluminum Laptop Stand,Aluminum Laptop Stand 17 Inch,Aluminum Laptop Stand Adjustable,etc.

Shenzhen Chengrong Technology Co.ltd is a high-quality enterprise specializing in metal stamping and CNC production for 12 years. The company mainly aims at the R&D, production and sales of Notebook Laptop Stands and Mobile Phone Stands. From the mold design and processing to machining and product surface oxidation, spraying treatment etc ,integration can fully meet the various processing needs of customers. Have a complete and scientific quality management system, strength and product quality are recognized and trusted by the industry, to meet changing economic and social needs .

Aluminum Laptop Cooling Stand,Aluminum Laptop Stand,Aluminum Laptop Stand 17 Inch,Aluminum Laptop Stand Adjustable

Shenzhen ChengRong Technology Co.,Ltd. , https://www.dglaptopstandsupplier.com